On 28 November, Thailand’s Prime Minister announced that the country would only open to substantial tourism once a vaccine was approved, produced and implemented. Now being a vaccine-dependent country, Thailand will rely heavily on domestic demand in the meantime. So where does that leave hotel performance?

While overall levels are still low, the country is reporting higher month-to-month performance, especially compared with nine months ago.

Thailand’s hotel occupancy dropped to a single-digit low in April (7.8%) and has since climbed its way back to 25.5% in November—the highest level in the metric since March.

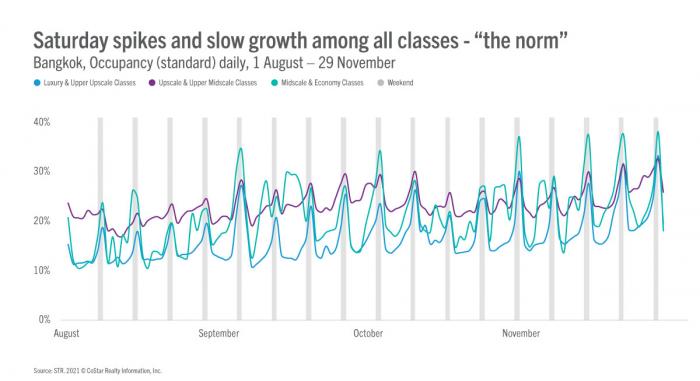

When looking at Thailand’s capital city, Bangkok, the lowest occupancy level in the market was also seen in April (10.8%). Occupancy stayed below the 20% level throughout the summer, eventually surpassing that threshold in October (21.2%), while November was slightly higher at 22.8%.

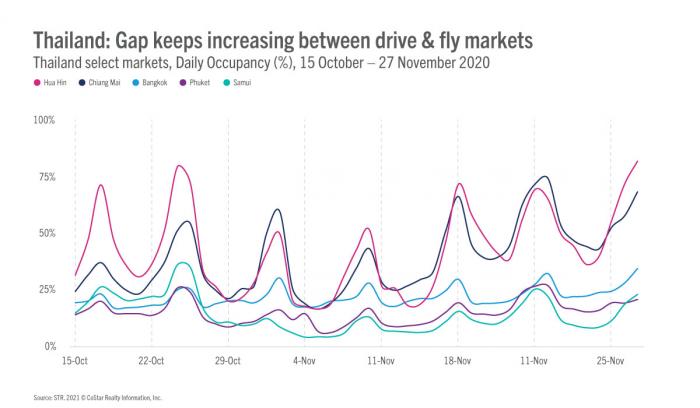

Phuket, on the other hand, remains under the 20% level, with November occupancy coming in at 16.3%. In other markets such as Chiang Mai and Pattaya Area, October occupancy levels reached 47.3% and 35.1%, respectively.

Weekly breakdown

Like other countries around the world, weekend demand has been the driver of occupancy for Thailand. While hovering in the 20% occupancy range during the weekdays, the country has seen spikes as high as 35% on weekends. Drive-to markets in the country are also experiencing similar performance patterns, such as Hua Hin, which has seen higher weekend occupancy.