Previous MRM versions: 24 April | 1 May

Week ending 8 May

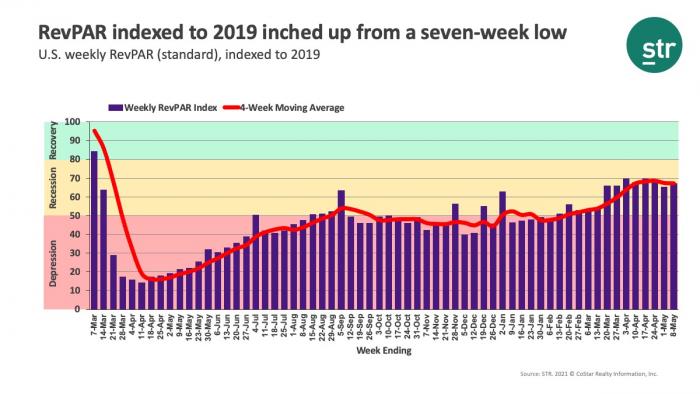

The occupancy doldrums remained in place with U.S. occupancy falling to an eight-week low (56.7%) during 2-8 May 2021. Using STR’s total-room-inventory (TRI) methodology, which considers hotels that are temporarily closed, occupancy dropped to 54.2%. Demand, however, increased slightly and remained above 21 million as it has since mid-March. The decrease in occupancy was a result of increased hotel openings. Supply was up 0.8% week over week with more than 284,000 additional rooms available this week than in the previous one. The weekly gain was the most since last summer.

The largest supply gains were in the New Jersey Shore market, where 28,000 rooms came online ahead of the summer season, and in Alaska. Among the Top 25 Markets, Washington, D.C., led the pack with the addition of 14,000 rooms followed by New York City. Chicago and San Francisco also saw openings during the week. Looking at the hotel stock by property size, large hotels (300+ rooms) continued to lag with only 93% of the rooms available in 2019 opened today. The other size categories were slightly ahead of the stock they had in 2019.

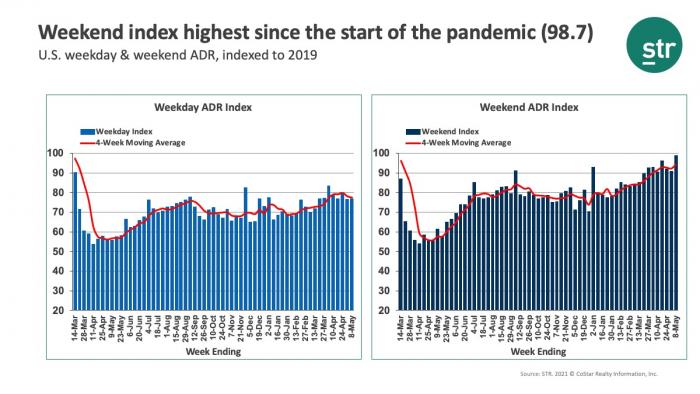

As mentioned, weekly demand increased but with notable differences. Weekday demand drove the increase and was up by its largest amount of the past month. More than 70% of all markets reported weekday demand gains with weekday occupancy increasing to 52% (50% TRI). Demand and occupancy in the Top 25 were also up with weekday occupancy at 50% for the week. Prior to this week, weekday demand in the Top 25 had fallen for four consecutive weeks. Occupancy for business hotels in urban locations in the Top 25 also increased to 43% after dropping in the previous week. While weekday performance was good, demand indexed to 2019 still has a way to go with this week’s figure dropping to 78.3, its lowest since mid-March.

Weekend demand fell by its largest amount of the past five weeks resulting in occupancy of 68% (64% TRI). Recall, weekend occupancy had been at or above 70% since early April. While we know supply gains played a role in this week’s overall occupancy softness, there is also seasonality at play. As compared with the same weekend in 2019, weekend demand came in with the second highest index (96) of the year, reflecting nearly identical performance during the comparable weekend from two years ago.

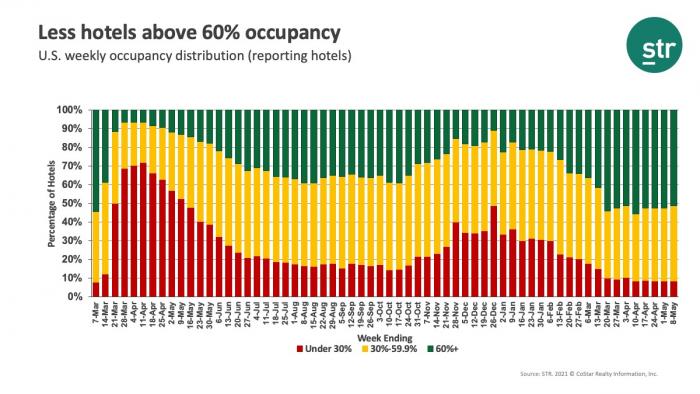

Occupancy distribution saw a slight change as less hotels had occupancy above 60% this week (51% this week versus 52% in the previous two weeks). There was also a slight rise in the number of hotels with occupancy below 30%. The 3,039 hotels with under 30% occupancy was the highest of the past three weeks but far better than the 14,000 in that category at the beginning of the year.